HomeBlogsCorporate sustainability reporting directing for food companies

Corporate sustainability reporting directing for food companies

Posted on:

Reading time:

The Corporate Sustainability Reporting Directive (CSRD) is a new European Union directive which requires large and listed companies to report on the financial risks they face for social and environmental matters as well as how they impact people and the planet.

In this blog, we will offer an overview of the CSRD and its requirements, focusing on two key aspects: the double materiality assessment and the European Sustainability Reporting Standards (ESRS), and including some key highlights for F&B businesses.

Towards the end of this article, you will find the contact details of a new partner of 1-2-Taste who can provide guidance to those directly affected by the CSRD or simply interested in voluntary disclosure on ESG (Environmental, Social, and Governance) topics.

Why should all food and beverage companies care about ESG?

Setting up a good ESG strategy and reporting is becoming increasingly more important for any company. This is definitely true for food companies because, among other factors, the agri-food systems’ emissions account for approximately 30% of total GHG emissions. Hence it’s a major contributor to climate change while also being strongly affected by this problem. Additionally, food waste and loss accounts for around 30% globally, and social challenges, especially in the agri sector are widespread. Therefore, whether you are obliged to comply with CSRD or not, setting up an ESG strategy and reporting is essential for any food business and it’s often requested by investors, customers and other business partners.

The guidance offered in this blog can be valuable for companies beyond the direct scope of CSRD. In fact, the new reporting standards set by the CSRD have been developed in tight collaboration with GRI (Global Reporting Initiative), the most widely used sustainability reporting standards globally.

Let’s start by clarifying some common abbreviations linked with CSRD.

NFRD (Non-Financial Reporting Directive): the CSRD is replacing the NFRD which was already requiring disclosure of non financial matters, but to a narrower group of companies and with a narrower scope. ESRS (European Sustainability Reporting Standards): the common standards that need to be used to report under the CSRD. They define what to report on and how. EFRAG (European Financial Reporting Advisory Group): an independent advisory board, which is mostly funded by the EU. They have been technical advisors to the EC in developing the ESRS.

Which F&B companies will be impacted by CSRD and from what date?

EU companies who fulfil at least two of the following criterias will need to comply:

• 50 million turnover • 25 million total assets • 250 employees

Additionally, the regulation applies to: Non-EU companies with large or listed subsidiaries in the EU generating over €150 million turnover within the Union for the last 2 financial years.

The time for compliance apply as follow:

• First report in 2025 for the financial year 2024: applies to companies previously affected by NFRD. • First report in 2026 for the financial year 2025: applies to large companies meeting the criterias, but not currently subject to the NFRD. • First report in 2027 for the financial year 2026: applies to listed SMEs, who can postpone the reporting until 2028. • First report in 2029 for the financial year 2028: for third countries companies.

And what about non listed SMEs? Non listed SMEs are not directly affected by the CSRD. However, EFRAG is working on voluntary standards that these companies can adopt. The standards are currently in the consultation phase until May 21st and can be accessed here.

Understanding the concept of double materiality

One fundamental concept underlying the CSRD is “double materiality”. The materiality assessment is the process used to determine the relevant matters a company should report on in terms of sustainability impacts, risks and opportunities.The term “double” refers to the fact that the assessment needs to look at how sustainability issues may affect their company (‘outside-in risks’), as well as how the company affects society and environment (‘inside-out risks’). The company should report on all the impact, risk and opportunities (IROs) which are found to be material (aka relevant) from a financial perspective (outside-in), impact perspective (inside-out) or both.

There is no mandatory set process for the double materiality assessment, but to meet ESRS requirements, the process should include:

• An explanation of the context • Identification of actual and potential impacts, risks and opportunities in relation to sustainability matters • Assessment of material IROs related to sustainability matters • Reporting on them

In order to identify actual and potential impacts and prioritise them for reporting, a company will need to engage with its stakeholders, like employees, investors, and customers. Suppliers, including farmers, also represent key stakeholders for food and beverage companies. The engagement can be done in a number of different ways including surveys, focus groups and more. Following the stakeholder engagement, the company will define what to report on based on the severity and likelihood of the impacts, risks and opportunities identified.

The process used to conduct the double materiality assessment needs to be disclosed as part of the general disclosure (ESRS 2 IRO1). Additionally, within the ESRS 2, general disclosure, the company needs to show the interaction between IROs and its own strategy and business model (ESRS 2 SBM3), as well as the disclosure for each of the sustainability statements (ESRS 2 IRO2).

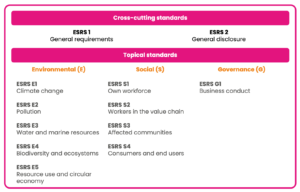

ESRS 1 (general requirements) defines the principles for reporting, the architecture of the ESRS and the basic concepts used.

ESRS 2 (general disclosure) is the other cross cutting standard, which is mandatory for all the companies affected by CSRD as presented in the last section.

10 topical standards, marketed with the letters “E”, “S” and “G”, because they are linked with the three areas of ESG (as presented in the table). These standards are subject to materiality. However, it doesn’t mean that these standards are voluntary. In fact, if a company does not report on a certain ESRS, let’s say ESRS E2 pollution, they will need to clearly justify – showing the process and result of the double materiality assessment – why the topic is not material to their company.

In addition, specific standards by sector were part of the ESRS proposal, and included ESRS for the food and beverage sector. However, on February 8th 2024, the European Parliament and the Council agreed to postpone the adoption of these standards from mid-2024 to mid-2026.

Within each standard, there are different data points (DPs) broken down by “shall” and “may”, indicating whether they are mandatory or voluntary to report on a certain ESRS. It’s important to always check the latest update from EFRAG on mandatory data points as changes are still ongoing.

So where should you start on your CSRD compliance as a food business and how should we manage the multiple ESG requests?

Even beyond CSRD compliance, the World of ESG is pretty complex. Stakeholders, including customers and investors, have diverse requirements, leading companies to spend considerable time and efforts understanding what to prioritise and how to communicate their impact effectively. To help food companies address this challenge, we’ve partnered up with VULCANO IMPACT, sustainability managers on demand, who can help you to navigate the complexity of ESG strategy, reporting, and certifications to streamline processes and reduce costs. Thanks to our partnership with them, you can book a free 20-minute ESG session, no strings attached. Click here to book the session.